Successful investing isn’t about chasing the latest trend or picking the “perfect” product. It’s about having a clear, well-thought-out strategy — and sticking to it.

Think of investing like building a house. The products you choose are the bricks and materials, but your strategy is the blueprint. Without the right blueprint, even the best materials won’t deliver the outcome you want.

Here’s how we approach investing on your behalf.

Strategy Comes First — Always

We don’t start with products. We start with you.

Your goals, timeframes and financial situation shape a tailored investment strategy. From there, we select investments that align with that plan — not the other way around.

Because in our experience, a strong strategy will outperform a collection of disconnected investment choices every time.

It’s About What You Keep, Not Just What You Earn

It’s easy to focus on fees alone, but the real measure of success is net returns — what actually ends up in your pocket after costs, taxes, and market movements.

A lower-cost option isn’t always better if it delivers weaker long-term outcomes. Our role is to find the right balance, ensuring your investments are working as efficiently as possible for you.

One of the most important decisions in investing is how your portfolio is structured across different asset classes.

Research and experience consistently show that strategic and tactical asset allocation is responsible for the majority of investment returns — often around 85%.

This is why we focus heavily on getting this right. It’s not about reacting to short-term market noise, but building a portfolio that is designed to perform across cycles.

Finding Opportunities Where Others Aren’t Looking

Large, well-known companies tend to be highly researched and efficiently priced. But in smaller companies, there are often more opportunities for skilled managers to uncover hidden value.

That’s why we include exposure to areas of the market where inefficiencies exist — giving you access to growth potential beyond the obvious.

Diversification — With Purpose

Diversification is a key part of managing risk, but it’s not about owning a little bit of everything.

We believe diversification should be intentional — spreading investments in a way that enhances returns while still protecting your portfolio. Over-diversifying can dilute performance, so we strike the right balance between protection and growth.

Using Gearing Strategically

When used responsibly, gearing (borrowing to invest) can enhance long-term returns.

It’s not about taking unnecessary risks — it’s about applying smart leverage in a controlled, thoughtful way to help build wealth more effectively over time.

A Long-Term Mindset Wins

Markets move. Headlines change. Emotions can run high.

But one principle remains constant: long-term investing delivers results.

Frequent trading not only increases costs but can also create unnecessary tax consequences. That’s why we focus on staying invested, maintaining discipline, and letting time do the heavy lifting.

Bringing It All Together

Our investment philosophy is built on clarity, discipline, and purpose:

Start with strategy

Focus on net outcomes

Structure portfolios intelligently

Seek out genuine opportunities

Manage risk without sacrificing growth

Stay focused on the long term

Because investing isn’t about reacting — it’s about planning.

The New Era Difference

We’re here to simplify the complex, guide you with confidence, and help you make smarter financial decisions every step of the way. If you ever feel unsure about the markets or your strategy, that’s exactly when a clear philosophy matters most.

Member Profile: Plasterer & lawyer, 31 & 27, Melbourne Starting position: Good income, had their first home, some ETFs & Bitcoin, but feeling uncertain about priorities and progress

Tim & Amanda were earning well and had made a solid start—buying their first home and having some ETFs and Bitcoin. Yet, they felt overwhelmed by competing priorities: saving for a wedding, planning a family, and wanting to be financially independent by 50.

They worried about whether their money was working hard enough, if they were missing opportunities, and how to balance enjoying life now with building for the future. They’d tried budgeting apps and ad hoc advice, but nothing stuck.

The Stakes

Without a clear plan, Tim & Amanda risked drifting financially for another decade—potentially missing out on wealth-building opportunities and delaying key life milestones like starting a family or upgrading their home. The emotional cost was ongoing stress and uncertainty, despite their strong earning power.

The Turning Point

They decided to seek help when they realised their current approach wasn’t delivering clarity or confidence. They wanted an adviser who could simplify complexity, provide structure, and help them align as a couple. Our outcome-focused, step-by-step process stood out as practical and supportive.

The Strategy

Discovery & Clarity: Deep dive into their goals, values, and current financial position.

Diagnosis: Identified gaps—such as underutilised cash reserves, overlapping loan structures, and unclear savings priorities.

Strategic Recommendations:

Prioritise emergency savings

Optimise loan repayments

Set clear, ranked goals (e.g., wedding, family, travel, home upgrade, financial independence)

Implementation Support: Provided tools, regular check-ins, and accountability.

The Implementation

We helped Tim & Amanda:

Rank and personalise their top goals, from Upgrading their home to Planning their Wedding and Annual holidays, while building towards financial independence

Automate savings for specific goals (e.g., wedding, new car)

Provided ongoing support to adjust as life changed

The Results

Quantitative:

Purchased an investment property & have used the equity in their home to build an investment fund

Improved their savings rate to 26.9%

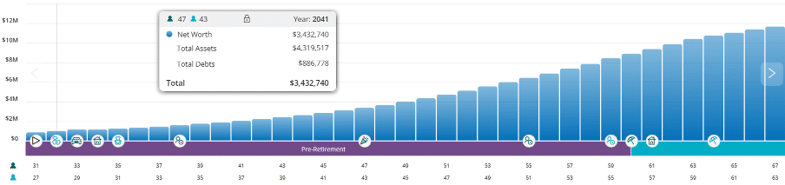

Net worth grew by $296,179 (a 76.1% increase)

Reduced debt-to-income ratio, with clear loan repayment plans

On track to achieve financial independence (debt free & passive income to cover their expenses when Tim is 47

Projected to have a net worth of $10,764,513 in their early 60

Projected to have a net worth of $10,764,513 in their early 60s

Qualitative:

Greater confidence and peace of mind

Reduced financial stress and arguments

Clear alignment on priorities as a couple

The Bigger Picture

With a strong foundation, Tim & Amanda are now planning for their next phase—starting a family, upgrading their home, and building wealth for the long term. Our ongoing relationship means they have support and structure as life evolves.

Key Takeaways

Clarity beats complexity—knowing your numbers is empowering

Structure creates confidence—having a plan reduces stress

Early action compounds—small steps now lead to big results later

If this story feels familiar, our Financial Blueprint Program is designed to help you gain the same clarity & confidence.

Book a complimentary Life by Design call to see if this approach is right for you.

Ever feel like you’re earning good money but not really getting ahead?

You’re not alone. In fact, it’s one of the most common things we hear from families all over Australia.

The truth is, most people aren’t struggling because of a lack of income. They’re stuck because they haven’t built the right financial foundations.

At New Era, we work closely with busy families and ambitious couples—and we’ve found that long-term success usually comes down to hitting five key financial milestones before the age of 40. Think of these as checkpoints on the path to financial freedom.

Here they are:

✅ 1. Crystal-Clear Goals and Priorities

If you don’t know where you’re headed, how do you know if you’re on the right track?

Defining your financial goals isn’t just a nice-to-have—it’s essential. Whether it’s buying your dream home, setting up your kids’ education, or achieving work-optional living by 50, your goals give your income purpose and your plan direction.

Without clarity, you’ll default to drift. With clarity, you’ll move with intention.

✅ 2. A Proven Cashflow System

We’re not talking about a rigid budget that makes you feel guilty every time you buy a coffee.

We’re talking about a system that aligns your income, expenses, savings, and investments automatically. A well-designed cashflow system makes managing your money feel effortless. It removes stress, creates structure, and helps you consistently make progress—without needing to track every cent.

✅ 3. Your First $100k Invested

The first $100,000 is often the hardest—but it’s also the most important.

Whether it’s in superannuation, ETFs, shares or investment property, hitting that first milestone gets your money working for you. That’s when compounding steps in—your secret weapon for building long-term wealth.

Once your investments start earning their own income, the game starts to shift in your favour.

✅ 4. Insurance and Risk Management Sorted

This isn’t the exciting stuff—but it’s absolutely essential.

If something unexpected happened to you or your partner, would your family be okay financially? Having the right insurance in place protects your income, your lifestyle, and your long-term goals.

Think of it like a safety net under your financial trapeze. You hope you’ll never need it—but if you fall, you’ll be glad it’s there.

✅ 5. A Plan to Pay Off Bad Debt (and Use Good Debt Strategically)

Debt can either be a weight that holds you back or a lever that moves you forward.

Getting clear on what’s bad debt (like high-interest credit cards or personal loans) and what’s good debt (like strategic investment lending) is the key to moving faster without unnecessary risk. Done right, it can mean smarter tax outcomes and accelerated growth.

Where Are You Right Now?

Most families we speak to have ticked off one or two of these money milestones—but not all five. And that’s perfectly okay.

The first step is knowing where you are. The next step is taking action to close the gaps.

🎯 Want to find out how you’re tracking?

We offer a complimentary 15-minute strategy call where we’ll help you:

Pinpoint your current milestone

Identify the next right move for your financial goals

When it comes to financial advice, one size definitely doesn’t fit all. Many traditional financial advisors focus on high-net-worth clients, leaving everyday Australians without the guidance they need to build wealth and secure their future. At New Era Financial Planning, we’re changing that. Our approach is designed to be accessible, tailored, and forward-thinking—helping ambitious individuals and families take control of their finances, no matter where they’re starting from. So, what makes us different? Let’s dive in.

1. Accessibility for All Income Levels: Unlike traditional advisors who often cater to high-net-worth individuals, we are committed to providing high-quality, reliable financial advice to everyday Australians, regardless of income.

2. Membership-Based Model: We offer a subscription-based service, allowing our members to receive ongoing financial planning support without prohibitive upfront costs.

3. Comprehensive Financial Roadmaps: We create detailed financial roadmaps (we call it a Financial Blueprint), helping clients understand the implications of various financial decisions and guiding them toward their goals.

4. Tax Optimisation Strategies: We assist our members in maximising their tax entitlements while building investment portfolios, ensuring efficient tax management.

5. Income Management for Diverse Earners: Whether members are salaried professionals, self-employed, or juggling multiple gigs, we provide tailored strategies to optimise income & manage cashflow.

6. Automated Savings Structures: We help set up account structures that automate savings, simplifying money management and goal tracking.

7. Property Purchase Planning: One of our more popular services, we offer guidance on property purchases, including price & yield analysis, suburb selection, and identifying eligible grants and schemes.

8. Loan Planning and Brokerage Services: Our mortgaging broking partners assist with loan applications, determining borrowing capacities, required deposits, and selecting suitable banks.

9. Investment Portfolio Development: We provide strategies for building investment portfolios, even starting with modest amounts, to help members grow their wealth over time. The benefit of investing early allows the magic of compound to do its thing!

10. Superannuation Management: Not secy but super important! We help our members optimise their superannuation to enhance retirement outcomes and achieve financial freedom.

Summary – New Era Financial Planning vs the rest

New Era Financial Planning

Traditional Financial Advisors

Accessibility for All

High-quality advice for all Australians, regardless of how much money you have.

Often focused on high-net-worth individuals or those with substantial assets.

Membership-Based Model

Subscription-based service with no prohibitive upfront costs.

Typically charge high upfront fees or percentage-based fees on assets under management (AUM).

Comprehensive Financial Strategies & Roadmaps

Detailed, goal-oriented roadmaps to clarify financial decisions and outcomes.

Often limited to general advice without detailed future planning.

Tax Optimization Strategies

Guidance to maximize tax entitlements and ensure tax-efficient investments.

May not provide in-depth tax advice as part of their service.

Income Management for Diverse Earners

Tailored strategies for salaried, self-employed, and gig workers.

Primarily cater to traditional salaried clients.

Automated Savings Structures

Account setups to automate savings and simplify money management.

Rarely provide personalized assistance with savings automation.

Property Purchase Planning

Advice on price points, suburb selection, and grants/schemes eligibility.

Typically do not offer property-specific planning or guidance.

Loan Planning and Mortgage Advice

Support for loans via partnerships with mortgage brokers, including borrowing capacities and bank selection.

Often limited to referring clients to external brokers without ongoing support.

Investment Portfolio Development

Strategies to build portfolios starting with modest amounts, fostering long-term growth.

Focus more on large-scale investments, requiring significant initial capital.

Superannuation Management

Helps optimize superannuation for tax efficiency and better retirement outcomes.

Often provide general superannuation advice with limited personalization.

Conclusion

We have aimed to break away from the exclusivity and high costs of traditional financial advice by providing simple, accessible and affordable advice & guidance. At New Era Financial Planning, we believe financial advice should be practical, accessible, and empowering—not just for the wealthy, but for anyone ready to take charge of their financial future. Whether it’s simplifying your cash flow, optimising tax strategies, or building a smart investment portfolio, we provide the roadmap and support to help you get there.

Life Insurance helps protect against certain risks if something were to go wrong. You essentially pay an insurance company a certain amount (usually a monthly ‘premium’) for them to pay you an amount if you need to make a claim. This can be for your car, home, health and even life. For example, most people have home insurance, where an insurance company will pay a certain amount if something happens to your home, such as a fire that destroys it.

How does it work?

Insurance is a risk management strategy – you pay a monthly amount to an insurance agent for the ability to make a claim and have money paid in the event of something happening. Normally we take out insurances on things that we can’t fund ourselves, such as needing to rebuild your home in the case of a fire.

The way it works is usually like this: you take out an insurance policy with a company for a certain amount and to cover you against certain things happening (they might call these ‘events’) and pay a monthly or yearly cost to the insurance company in return for them agreeing to pay you a certain amount in the future if you need to make a claim.

Eg: You want to cover the cost of rebuilding your home if it is destroyed by flood, fire or hurricanes. You estimate it will cost $500,000 to do this so take out insurance to cover that amount. The cost of this is $1,000 per year, which you pay to the insurance company. You don’t get this back if you don’t make a claim, however you have the peace of mind that if something happens you can claim and the insurance provider will pay you out $500,000 to rebuild your home.

Types of cover – Life Insurance, TPD, Trauma & Income Protection

As financial planners we look at insurances as part of an overall risk management strategy. This strategy includes having an emergency fund, protecting things like your home, car & health, and then making sure that you are covered financially if you were to pass away or unable to work. These last types of cover fall into the ‘Life Insurance’ basket and are predominantly made up of the following:

Life Insurance: Pays you a certain amount of money (usually as a one off) if you pass away. The money will go to the people you nominate as your ‘beneficiaries’ (normally your partner and/or kids) and is usually used to pay off any outstanding loans, cover funeral expenses and provide some financial comfort for the family.

Total & Permanent Disability (TPD): This also pays you a one-off amount, but in this case if you are so seriously injured or unwell that you are unable to ever work again. This can get specific on when it will be paid out so it’s best to do your research or get some help, but the main idea is that if you can’t work anymore, for example due to a car accident or major illness, you will get a payout which can be used to clear any outstanding loans, help with medical & rehab costs, and provide some financial comfort to you and your family. There are 2 types of cover here:

Any occupation cover – this will pay out if you are unlikely to work again in any occupation that you are reasonably suited for based on training, qualifications and experience. It is slightly harder to claim under this option, however is slightly lower cost as a result.

Own occupation cover – this will pay out if you are unlikely to ever work again in your currentoccupation. It is easier to claim on this however is slightly more expenses, but in our opinion worth it!

Trauma/Critical Illness Insurance: This also pays out a one-off amount, but this is specifically if you suffer a serious illness, such as cancer, a heart attack or stroke. This type of cover is to help with your recovery and to pay for things like medical & rehab costs and some financial support while you are on the mend.

Income Protection: This pays part of your income if you’re unable to work because of a disability caused by illness or injury. It can help pay the bills so you can focus on getting better. It usually kicks in after 1-3 months of being sick, so isn’t necessarily to cover time off for things like colds. Income Protection can pay you for a certain amount of time (such as 2 years) or until you are back at work, whichever is the earliest.

Payout options: Most options pay you 70% of your income if you can’t work, however this amount can differ a little bit so is worthwhile getting help on your options. There is also what is known as a ‘benefit period’, which is basically how long you are paid for. You pre-select a timeframe that would be the maximum amount of time your get paid, such as 2 years, 5 years or until you are 65 years old. If you are able to go back to work within that timeframe then the payments will end as well, however if you are unable to go back to work after the benefit period ends you will need to look at other funding sources, such as the Disability Pension.

Waiting Periods: This is how long you wait until your income protection starts paying you once you make a claim. It is not like private health cover, which may have a 12 month waiting period before you can claim on certain items – most policies allow you to claim as soon as it is in place, however there are options have the monthly payout start 30-90 days after you are first sick/injured. The benefits of the longer ‘waiting period’ is a lower cost of insurance, however you need to make sure you have enough savings and/or sick leave to cover that period.

Payment options

These types of insurances can usually be paid either out of your bank account/credit card, like car & home insurances, or from your super fund. You may have some insurances inside your super fund already, however there are some restrictions on what types of insurance can be held within super, as well as the benefits payable and access of these. We usually like a mix of paying for insurances inside super and personally to get an ideal blend of affordability, tax benefits (for example income protection is usually tax deductible) and simplicity at claim time.

Our Insurance Philosophy

We look at insurances as part of an overall risk management strategy. This strategy includes having an emergency fund, protecting things like your home, car & health, and then making sure that you are covered financially if you were to pass away or unable to work. As a rule of thumb, we believe around 3% of your total household income is appropriate to spend on the ‘life insurance’ category, and around 5% of your income on total insurances (including car, home & health). This leaves you with 95% of your income to pay your mortgage & bills, save, invest & spend.

Our insurance philosophy is built around the idea that insurances are needed to put you back into the financial position that you would have been in if the event that occurred never happened. For example, what financial position would you & your family be in if you didn’t have to have time off work, or were diagnosed with cancer, or worst case passed away? This is largely based on the financial blueprint that we put together for people, however as a rule of thumb covers against the following:

If you pass away – leaving your family with enough to be debt free (the financial blueprint always aims to be debt free within a certain period) and support themselves for a few years

If you can’t ever work again – having enough to pay out your mortgage and any other debts and cover the medical, rehab & any other costs incurred due to the injury / illness.

If you suffer a serious illness – covering the medical, rehab & other costs associated with the illness.

Income Protection – covering your income while you are off work and recovering. This income is still needed to pay the bills, and there may be other medical expenses due to the injury or illness that need to be paid for as well.

Financial comfort – we usually look at some money to provide financial comfort & support on top of the above, so people don’t have to worry about money and can focus fully on recovering. Studies have shown that money-related stress can slow down the recovery of injury & illness, so we want to alleviate that as much as possible.

Types of risk that can affect your ability to earn an income and derail your financial plan

Unemployment

There isn’t any type of insurance that can protect against this. Instead we like to build cash reserves to utilise in these instances (3-6 months of living expenses), plus make sure you are always employable by improving your skills & training.

Accident/Illness or other Health issues

Short term (0-24 Months) – Ways to Get ready for short term:

Cash buffer (3-6 months living expense)

Sick leave

Insurances that pay out if you can’t get to your own job for a few months

Long term (24 Months & Beyond)

Insurance that will take away some big-ticket financial pressure e.g. debt, major medical and kids expense if you cant get back to your own job even after 2 years, as your current debt & Kids education plans is based on the income you generate in your current job, not based on a job an occupation therapist from the future, paid by an insurance company says you can do.

Insurances that pay out if you can’t get to any job for the foreseeable future

Having insurances Inside super vs Outside super – best of both worlds?

Some insurances can be held within your super fund, such as Life, TPD & Income Protection Covers. This can help with affordability of insurances, however some of the covers aren’t as good when held within super due to legislation requirements at claim time. For insurances held within super, they must meet the ‘Superannuation Industry Supervision Act’ (also known as ‘SIS’). In a nutshell, even though the insurance might pay out because you have made a claim, the super fund may not pay the money to you because you haven’t met one of the requirements to be paid. All insurances owned through super get ‘released’ (paid) to the super fund first – this is something most people don’t realise and is a little quirk of the system. So it is very important to make sure you will be able to get your money when you need it.

For each of the main covers:

Life insurance – This is usually ok to be held within super because at claim time it’s fairly straightforward (when you’re dead you’re dead!). If paid to your spouse or someone who is financially dependent on you the payout will be a tax-free lump sum regardless of if it’s through super or outside, and there isn’t any trouble with the super fund paying the money to your family as death is one way that you can access money from your super. The main downside when holding Life Cover through super is there are only certain people can be nominated as a beneficiary – essentially immediate family or someone who is dependent on you – and adult children may be taxed on the payout.

TPD – Here is where things start to get tricky. With TPD through super you can only make a claim if you are unable to work in any occupation that you have training, experience or qualifications in. When holding it outside you are able to have it set to claim on your own occupation, which means it is easier to claim. Because TPD cover is usually linked to Life cover though, it is usually easier to have it through super with life cover. So we generally like to ‘link’ the TPD inside super & outside to help with affordability and get the better claim ability at the same time.

Trauma – this cannot be held within super due to legislation, so is only able to be held and paid for personally.

Income Protection – Like TPD, things can get a bit murky here. There have been a lot of changes with Income Protection legislation recently and there are so many nuances within different policies now. They are all fairly streamlined in being able to claim a maximum of 70% of your income, however some policy can drop that amount depending on how long you are paid for. You can hold Income Protection through super, however we generally recommend that it is held outside because it is tax deductible, and it is a bit quicker at claim time because you get paid directly. For those that have affordability issues we as a minimum recommended the ‘linking’ of the Income Protection inside super and outside, like the TPD.

Paying for cover through super

For cover that you hold through super (usually life insurance & TPD), the cost will be taken from your super balance. For small amounts this may not be too much of an issue, however over time it can add up to large amounts and deplete your super balance. Due to this we like to recommend adding some extra to super to cover some or all of the costs. For example, this can be done by salary sacrifice, which also reduces the amount of tax you pay, or in a way where you qualify for a Government Co-Contribution if eligible, which can help pay some of the costs.

‘Super linking in more detail’

What is Super linking?

This is the ability to ‘link’ certain insurances (specifically TPD & Income Protection) inside super and outside. The reason people do this is to help pay for the insurances through super, whilst getting the better claim definitions outside super.

What is the benefit?

What is the SIS act’s condition of release – this is the techinal term for when your super fund can pay you your money and or insurances. By law super is to fund your retirement, so normally cannot be accessed until a certain age (currently at least 60) and also needing to be retired if you want to access your money between 60 & 65. There are a handful of other ways to access super early, with 2 of the main ones being death and permanent disability. If you have these insurances within super you will be assessed by both the insurance company on whether the claim is successful, and after that from the super fund on whether they are able to release the money from your fund. The insurance provider will have to pay the claim to your super fund, who will then decide whether they are allowed to pay you based on the laws of super access.

Legislative risk – there is a small risk of the insurance company paying a claim and the super fund deciding not to release the funds. Usually the risk is more that the insurer will deny the claim, especially in the case of the ‘any occupation’ TPD cover noted previously. A lot of super funds have this as standard; we generally recommend having the better ‘own occupation’ definition so increase the likelihood of the claim being successful.

Chance of claim – there is a better chance that you will be able to claim on the ‘Own occupation’ TPD definition, as it will kick in if you can’t work in your current job, not just any job you are qualified to do. Because of this we prefer this option and have built it into our insurance philosophy. Most super funds do not off er this option directly though, which is why it is important to look into the right provider and not just take the standard insurance that is offered through super.

Conclusion

Life insurance & the other types of cover can provide a great safety net for you, however we believe they are part of an overal risk management & financial plan. We aim to get the right blend of required cover, affordability & tax benefits with all the insurances that we look at.

So, what does a financial advisor do? It’s a common question we get, and the answer usually surprises people!

Managing your finances can feel overwhelming, especially when juggling life’s many responsibilities. That’s where a financial advisor steps in. A financial advisor helps individuals, families, and couples make informed financial decisions, guiding them toward achieving their financial goals with confidence and clarity.

The Role of a Financial Advisor

A financial advisor is more than just someone who helps with investments—they provide strategic financial guidance tailored to your personal circumstances and aspirations. In Australia, financial advisors operate under strict regulations & guideline set by ASIC (Australian Securities and Investments Commission) to ensure they act in their clients’ best interests.

What does a Financial Advisor do – the Key Services

Financial advisors offer a broad range of services designed to support your financial well-being, including:

1. Goals Planning

Help articulate what you want out of life, both financially and personally.

Define short-term and long-term goals to create a clear financial roadmap.

Align financial strategies with your values and aspirations.

2. Strategy Development and Modelling

Utilise detailed financial modelling to illustrate different pathways to achieving your goals. This could be thing like should you keep your current home when we upgrade, or should you invest in shares, property or through super? A detailed strategy is like a financial blueprint that will outline the right path for you based on what you want to achieve.

Provide tools to adapt your financial plan as life circumstances change.

Ensure ongoing adjustments to optimise financial success over time.

3. Wealth Creation and Investment Advice

Develop personalised investment strategies aligned with your risk tolerance and goals.

Provide insights into shares, managed funds, property investment, and other asset classes.

Monitor and adjust your investment portfolio to maximise returns over time.

4. Superannuation and Retirement Planning

Help optimise your superannuation to ensure a comfortable retirement.

Advise on the different types of super funds & contribution options and how they fit into your wealth strategy.

Create retirement income strategies that provide financial security.

5. Personal Insurance and Risk Management

Assess your insurance needs, including life, total and permanent disability (TPD), trauma, and income protection insurance.

Ensure you and your family are financially protected in case of unexpected events.

6. Debt Management and Cash Flow Planning

Develop strategies to reduce debt faster and more efficiently.

Help structure loans and mortgages to improve financial flexibility.

Create a cash flow plan to ensure you’re living within your means while still growing your wealth.

7. Estate Planning and Wealth Transfer

Work with legal professionals to ensure your assets are distributed according to your wishes.

Provide strategies to minimise tax implications and protect your family’s financial future.

The Outcomes of Working with a Financial Advisor

Partnering with a financial advisor can lead to several long-term benefits, such as:

Peace of mind: Knowing you have a structured financial plan gives you confidence in your financial future.

Increased wealth: Strategic investment and tax-effective planning help grow your assets over time.

Financial security: Proper insurance coverage and estate planning protect your loved ones.

More free time: With an expert handling your finances, you can focus on what truly matters—your family, career, and passions.

Is It Time to Speak with a Financial Advisor?

Whether you’re starting out, building wealth, or preparing for retirement, a financial advisor can provide valuable guidance tailored to your needs. At New Era Financial Planning, we work with clients across Australia to create personalised strategies that help them achieve financial success.

If you’re ready to take control of your financial future, get in touch with our team today. Let’s build a roadmap to your financial goals—together.

Ready to take control of your money?

Kick off your no-obligation trial today – book your 15 minute discovery call